General Manager Borgun

Questioning of General Manager for Acquiring of Borgun

September 25, 2024

1769516419

Dark Mode

Today there was a hearing of a witness from Borgun in the Wirecard courtroom.

There were some important and interesting statements from the witness, who was the general manager at Borgun responsible for acquiring exclusively international customers.

More about Borgun here:

crunchbase.com/organization/borgun

More about Borgun here:

crunchbase.com/organization/borgun

The questions of Dr. Braun's public defender were on the whole rather unspectacular, often very general and not very coherent.

It shines through that a further lack of understanding of coherent questions also for the public with brief explanations of the consequences of the questions to witnesses seems to be a shortcoming of the defense attorneys as a whole.

It shines through that a further lack of understanding of coherent questions also for the public with brief explanations of the consequences of the questions to witnesses seems to be a shortcoming of the defense attorneys as a whole.

Oliver Bellenhaus asked a few questions, he was particularly interested in the topic of rolling reserve, as well as fees for regional and international payment transactions. Bellenhaus asked how the fees would change if payment processing were moved from the UK to Singapore. Answer: from 0.3% to 3%.

Dr. Braun then asked Borgun's witness a few questions in person. It became so quiet and exciting that you could almost hear the quiet typing of a single journalist in the room from the press galleries.

Dr. Braun began with his first question, asking whether the Borgun witness knew the total acquiring volume handled by his company in 2016/17.

The witness could not or would not answer this, not even as a rough estimate, as he stated that he was only "responsible for international partner companies abroad" (Borgun was founded in Iceland).

The witness could not or would not answer this, not even as a rough estimate, as he stated that he was only "responsible for international partner companies abroad" (Borgun was founded in Iceland).

Dr. Braun asks further questions about two companies, InterConsult and PayVision, the ex Wirecard CEO wants to know from the witness who was behind InterConsult.

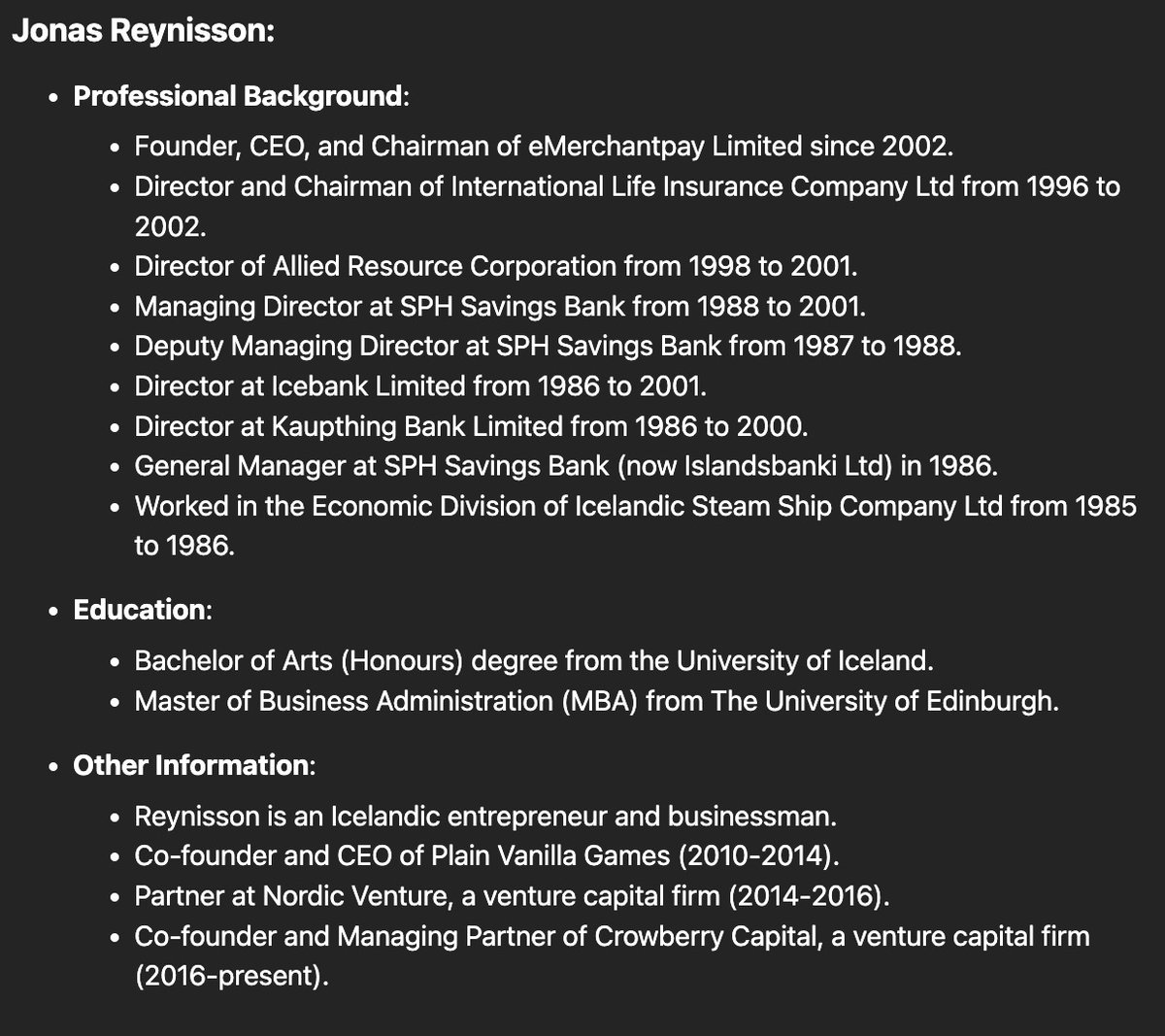

The witness said that it was a certain Jonas Reynisson.

Braun went on to ask whether InterConsult had additional partners besides Agora, and the witness answered in the affirmative.

The witness said that it was a certain Jonas Reynisson.

Braun went on to ask whether InterConsult had additional partners besides Agora, and the witness answered in the affirmative.

Dr. Braun went on to ask whether the witness knew how high the high-risk volume at Borgun was; the Wirecard witness replied around 40% in his international division.

Braun goes on to ask whether there was a real KYC check, i.e. whether Consett traders were checked themselves or whether the information was simply taken over when a trader switched to Borgun.

The witness says that they only took over existing information.

So "no assignment was made that, for example, a concept company was really a completely different one," says Braun.

Braun goes on to ask whether there was a real KYC check, i.e. whether Consett traders were checked themselves or whether the information was simply taken over when a trader switched to Borgun.

The witness says that they only took over existing information.

So "no assignment was made that, for example, a concept company was really a completely different one," says Braun.

Now it gets exciting, because Dr. Braun asks the witness whether he knows where PayVision comes from, from which region.

The Wirecard witness answers: Amsterdam, he had met their people there.

The Wirecard witness answers: Amsterdam, he had met their people there.

Dr. Braun then reads out an email from Borgun's Fionn Stakelum to Wirecard's Jan Marsalek:

"Before I answer, I wanted to see what you think. This proposal gives us the opportunity to use Borgun without getting into compliance issues and being involved in challenges, nevertheless we can charge a fee for our gateway, in addition we will receive commissions, this will be based on a rate of 2.8%, but it will be called differently. I think this is not only a good option for the cold merchant case, but for all future occasions".

Dr. Braun asks the witness if he is aware of such a thing. The witness says no.

"Before I answer, I wanted to see what you think. This proposal gives us the opportunity to use Borgun without getting into compliance issues and being involved in challenges, nevertheless we can charge a fee for our gateway, in addition we will receive commissions, this will be based on a rate of 2.8%, but it will be called differently. I think this is not only a good option for the cold merchant case, but for all future occasions".

Dr. Braun asks the witness if he is aware of such a thing. The witness says no.

Dr. Braun goes on to ask whether the Wirecard witness is aware of such a thing as a "buy rate".

The Borgun witness replied that instead of splitting profits, an agreement was made with the partner in order to be paid, and that "the profit was transferred to the partner" (!).

The Borgun witness replied that instead of splitting profits, an agreement was made with the partner in order to be paid, and that "the profit was transferred to the partner" (!).

An interesting Wirecard question/answer ping-pong then develops between Dr. Braun and the witness:

Braun: What exactly happens with a buy rate ?

Witness: We calculate the merchant revenue, we don't calculate a 50/50 split but keep the buy rate, the rest goes to the partner, we always pay the merchant and the commission to the partner.

Braun: But you don't know which commission goes to the partner!

Witness: If we have a partner, we know the commission, if it's a payment facilitator, then we have no idea (!).

Braun: So you simply deduct the 2.8%?

Witness: No, only if the buy rate is agreed as a contract, commissions are deducted from the merchant and the rest goes to the partner. A payment facilitator is something like a merchant, they settle with sub-merchants who have a buy rate.

Braun: What exactly happens with a buy rate ?

Witness: We calculate the merchant revenue, we don't calculate a 50/50 split but keep the buy rate, the rest goes to the partner, we always pay the merchant and the commission to the partner.

Braun: But you don't know which commission goes to the partner!

Witness: If we have a partner, we know the commission, if it's a payment facilitator, then we have no idea (!).

Braun: So you simply deduct the 2.8%?

Witness: No, only if the buy rate is agreed as a contract, commissions are deducted from the merchant and the rest goes to the partner. A payment facilitator is something like a merchant, they settle with sub-merchants who have a buy rate.

Dr. Braun would now like to go through things with a concrete example with a merchant/partner JustRock Inc. (?) with the witness, which was processed via Borgun in February 2017/2018. Unfortunately, the Wirecard witness said that he did not know JustRock Inc.

Braun: Does Sata Bank mean anything to you?

Witness: No.

Braun: Does Sata Bank mean anything to you?

Witness: No.

Now actually comes the kicker, as Dr. Braun now briefly explains in the Wirecard courtroom that he had asked for all this "because some of the payments flow into Pittodrie Finance, including those of a Consett company".

Von Erffa's lawyer asked 2.3 more questions, after which the witness was released unsworn.

Update after reference to point 7/:

The former director of Interconsult International Ltd. was named by the Borgun employee and Wirecard witness as Jonas Reynisson.

The former director of Interconsult International Ltd. was named by the Borgun employee and Wirecard witness as Jonas Reynisson.

Details on Jonas Reynisson:

Leave a comment:

Send

Send

Recommended:

October 9, 2025

The eBay Laptop

A Bavarian crown witness and missing Swiss data

September 1, 2025

The Uncles’ CIA Rogue Fixer

Jan Marsalek's double life the Financial Times just overlooked

July 31, 2025

The Final Blast

A Wirecard court summer break summary

April 4, 2025

The Implosion

About winter end time weeks in the Wirecard courtroom

January 18, 2025

The Justice Colleague Ping-Pong

About a weird back and forth in the Wirecard court process

September 17, 2024

Wirecard Sacked

The Court Proceeding - Season 1, Episode 1

August 25, 2024

The Wirecard Summer Gap

About extorted confessions and Bavarian radio news

July 22, 2024

Hotel Wirecard

About broccoli and roastbeef in Munich hotel rooms

June 28, 2024

Money launding is not my thing

About Commerzbank and cancelled Wirecard credit lines

July 3, 2024

Wirecard Chances

About supervisory board advising lawyers

June 20, 2024

The Wirecard PR Court

About an obscure questioning of a Wirecard lawyer

May 15, 2024

Wirecard Rogue

About crazy judiciary talks and on-target court motions

May 25, 2024

Wirecard Untangled

About unsolved issues in Germany's master finance scandal

April 29, 2024

All Inside The Singapore Folder

About Wirecard book keepings an email conversations

April 25, 2024

Grand Vision Trust

A Wirecard Bank Director and Relationship Managements

April 19, 2024

Mount Interim

About a Wirecard interim-CEO on a Swiss rose mountain

April 3, 2024

Harvesting Wirecard

About Swiss roses and Wirecard bears

March 29, 2024

The PayLondon Group

About bears from London and Wirecard targetings

March 24, 2024

Mount Acronis

About a Swiss IT sponsor and Wirecard entanglements

March 15, 2024

Magic Pav

About a Wirecard whistleblower and magic law firms

February 13, 2024

The Trial

About a Wirecard release of prisoner and Franz Kafka's unfinished works

October 4, 2023

Mount Wirecard

About Swiss Wirecard entanglements and the remains of Crypto AG

August 22, 2023

Wirecard Court Halftime

About seven months in Munich Stadelheim and the miracle of Bern

May 18, 2023

Pandora's Box

About Wirecard's IT Architectures

April 29, 2023

The Third Man

About Wirecard's interim CEO James Freis and nice shoes

December 8, 2022

Deflective Attorneys

About a five hours Wirecard indictment

February 18, 2021

Bavariacard

About a Germanic Wirecard Poker

May 5, 2021

A Munich Fraud

Wirecard and Munich's Public Prosecutor's Office

November 22, 2021

Royal Courts of Wirecard

About a Wirecard Lawsuit and Quantum Physics

October 1, 2021

Brilliant Consultants

About Wirecard's financial auditors and the chess game

November 6, 2021

Back To The Wirecard

About the roots of the insolvent German payment provider

April 15, 2021